|

November 27, 2023 – In this issue you’ll find news on states working towards a consistent benefit-cost analysis (BCA) framework for all distributed energy resources (DERs), and how the National Standard Practice Manual (NSPM) can be applied in different regulatory contexts. Learn about the treatment of federal tax incentives in BCAs, and how California’s Total System Benefits (TSB) approach fits within the NSPM framework. Finally, read about the forthcoming US DOE guide on how to conduct a Distributional Equity Analysis (DEA) alongside a BCA to inform DER investment decisions. I hope you find this issue informative. As always, your feedback is welcome.

— Julie Michals, Director

|

| |

--Featured States: Michigan & Maryland

--NSPM for NWAs, T&D Plans and More

--Federal Tax Incentives in BCA

| | |

--Unpacking CA's TSB Metric and NSPM

--Key Stages of a DEA

--Upcoming Events

| | Featured States Using the NSPM | | |

The most recent NESP News featured Minnesota’s new process using the NSPM BCA Framework to develop a “MN Cost Test” for utilities to apply in their next Conservation Improvement Program (CIP) Triennial Plans.

Now we highlight Michigan and Maryland to illustrate how states can develop a consistent cost-effectiveness test for all DERs using the NSPM, but where regulatory processes may differ.

| | |

In Michigan (Case U-20898), the commission required that the utilities develop a proposed BCA for DER pilot programs using the NSPM; the utilities then submitted a proposed jurisdiction specific test (JST) using the NSPM 5-step process; stakeholders responded with written comments on the utilities’ proposed JST, and with consideration of those comments, the commission issued a final order to adopt a new cost-effectiveness test for all DERs.

| | |

In Maryland, the commission opened Case No. 9674 to develop a unified BCA (UBCA), and convened a facilitated workgroup and series of workgroup meetings to follow the NSPM 5-step process whereby stakeholders inform each NSPM step to ensure consistency with the NSPM BCA Principles. This process is still underway. The workgroup’s intended outcome is to reach consensus on a proposed consistent UBCA for commission staff to file for approval.

Read more to learn about these state processes and key issues addressed.

| |

NSPM and Non-Wires Alternatives, T&D Plans and More

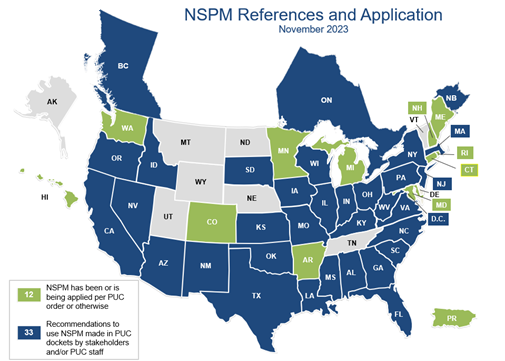

| | The NSPM is informing cost-effectiveness analysis of DERs in 12 states, and it has been referenced or recommended in another 30 states (plus three Canadian provinces). | | |

State examples show how NSPM guidance is being referenced or recommended, e.g., in the context of evaluating investments in non-wires alternatives, transmission and distribution plans, or informing discount rate selection:

Illinois Docket 22-0486 / 23-0055. The Environmental Defense Fund submitted comments on Commonwealth Edison Company’s Multi-Year Grid Plan and Rate Plan, where EDF agreed with ComEd on the need for a new cost-benefit analysis tool for non-wires alternatives. EDF recommended that the Illinois Corporation Commission (ICC) require that ComEd develop a jurisdiction specific benefit-cost framework using the NSPM. (Pages 94-95) The ICC‘s Proposed Order recognizes the need to standardize the approach for evaluating benefits and costs of future Grid Plans, and directs ComEd to engage in discussions with interested stakeholders regarding the categories of benefits and costs that should be considered, the method of calculating them, the proceedings to which those calculations are relevant, and other questions. At the conclusion of those discussions among stakeholders, and especially if consensus is not reached, the Commission may open a proceeding to formalize a BCA approach. (Page 306)

Maine Docket 2022-00322. In its Procedural Order and Request for Comment, the Maine Public Utilities Commission asked stakeholders how to identify priorities regarding transmission and distribution (T&D) plan filings. One question was how the commission should evaluate the cost effectiveness of T&D investments. The joint comments of Acadia Center, Conservation Law Foundation, Maine Conservation Voters, Natural Resources Council of Maine, and the Union of Concerned Scientists suggest using an NSPM process to modify existing BCA practices. (Pages 7-8)

South Dakota Docket EL23-019. When Otter Tail Power Company applied for approval of its 2024-2026 Energy Efficiency Plan, it used NSPM guidance plus experience in Minnesota to propose an updated discount rate. (Otter Tail Power operates in both SD and MN.) Otter Tail Power uses a Total Resource Cost Test (TRC) and had previously used a weighted average cost of capital (WACC) discount rate of 7.09 percent in SD. In MN where the NSPM was applied to develop a Minnesota jurisdiction specific test, a societal discount rate of 3.3% was applied. Otter Tail Power explained in its response to commission staff questions on its EE Plan that a blended discount rate more accurately reflects both the utility and customer costs of capital (i.e., the spending position of both the utility and the utility customers who ultimately fund programs and equipment). As a result, Otter Tail Power changed the discount rate they were using for their TRC in SD to 5.2%, an average of the 7.09% discount rate and the 3.3% discount rate, to reflect the perspective of both the utility and the customers.

| | Accounting for Tax Incentives in BCAs | | Forthcoming White Paper by NESP | | |

Guest Writer: Melissa Whited, Synapse Energy Economics

Benefit-cost analysis (BCA) is a powerful tool for helping jurisdictions identify optimal levels of DERs. Some of the impacts included in a BCA test can be described as “transfers” between two different parties, and they require special attention. Tax incentives are a prime example of a transfer, where the benefits to the DER host customers are exactly equal to the costs to taxpayers. Should such transfers be considered both a benefit and a cost? Should they be excluded from the BCA altogether because they cancel each other out? Should they be treated only as a benefit, or only as a cost? With recent federal legislation providing significant tax incentives to customers for installing DERs, the answers to these questions will have important implications for BCA and the determination of which DERs are cost-effective.

The answer to these questions lies in the perspective taken in the BCA. For example, under the traditional Societal Cost Test, both entities (the host customers and the taxpayers) are members of society, so the transfer of tax revenue from one entity to another typically has no overall impact on the net benefits of the BCA. However, jurisdictions might not use the Societal Cost Test as the primary means of identifying the net impacts of investments in DERs. As discussed in the NSPM for DERs, each jurisdiction should define its primary cost-effectiveness test in a manner that accounts for the jurisdiction’s applicable policy goals and objectives.

What does this mean in terms of accounting for transfers like taxes in a BCA? The short answer is that it depends on how the jurisdiction defines the scope of its BCA test. Are the regulators in the jurisdiction required to consider the impacts on all entities, including those in other jurisdictions? Is it the regulator’s responsibility to treat taxpayers equivalently to ratepayers? The answers to these types of questions will help define how off-setting impacts are accounted for in the jurisdiction’s BCA.

While the NSPM for DERs (Appendix F) addresses the topic of how to treat transfers in BCA, Synapse will take a deeper dive into this complex topic in a forthcoming paper being prepared for the NESP.

| | Unpacking CA’s Total System Benefits Metric and the NSPM | | |

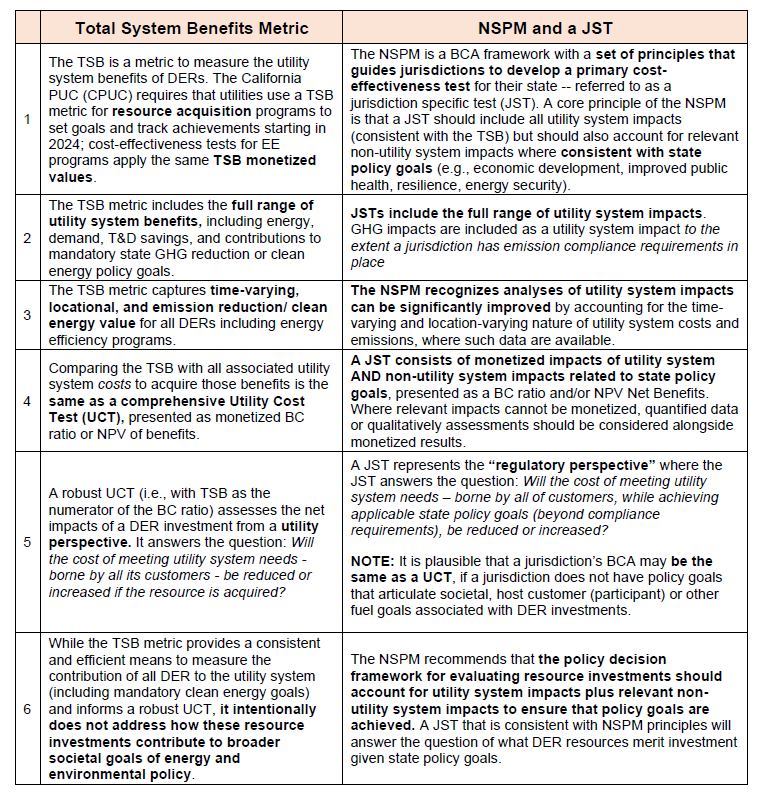

Last month, I had the opportunity to chat with Mohit Chhabra of NRDC about the total system benefits (TSB) metric, adopted by California, vis a vis the NSPM BCA framework. Mohit had just given an excellent presentation on the TSB metric at ACEEE’s Efficiency as a Resource conference in Philly, after which we discussed the distinction between the TSB metric and a jurisdiction specific test (or JST), developed using NSPM BCA framework and foundational principles. With the help of Chris Neme (Energy Futures Group), we compared the relationship between the TSB metric and a JST, listing distinctions reflected in the table below.

In sum, the TSB and the JST are both necessary. They help policymakers answer different critical questions: The TSB metric measures DER benefits from a utility point of view; this includes contribution towards complying with mandatory clean energy goals. The JST brings clarity to assessing the amount and mix of DERs that is consistent with state policy goals.

Both the TSB and the JST support consistent valuation of all DERs, thereby reducing inefficiencies and potential misallocation of resources otherwise caused by fragmented DER valuation and procurement.

| | |

With agreement on the six key points above, we also discussed where and how the TSB metric and JST address equity and support for low-income utility customers.

In CA, where the TSB metric is being applied in the context of resource acquisition programs, the CPUC requires 30% of efficiency funds be used for equity focused programs that serve hard to reach customers and businesses in disadvantaged communities. No BCA is currently required, but metrics (in development, expected Q2 2024) will be applied. This is in addition to Energy Savings Assistance programs provided to qualifying low-income residential customers (the budgets for these programs are determined through a separate application).

The NSPM does not address separate funding carve-outs for low-income programs, but it does recognize that some states use “alternative thresholds” for low-income BCAs, where no BCA is required or where a BC ratio of < 1.0 is acceptable.

Regarding the issue of equity and the distribution of benefits and costs of DER investments across customer groups (e.g., priority populations vs all other customers), BCA does not address equity. Rather, a distributional equity analysis (DEA) is needed, alongside a BCA, to understand the equity implications of DER investments. See separate article “Distributional Equity Analysis for Energy Efficiency and Other Distributed Energy Resources – A Practical Guide."

Summary

In conclusion, both a JST and a UCT (reflecting TSB) are important BCA tests to inform DER investment decisions, recognizing they answer different questions. We agreed that a BCA decision framework for evaluating resource investments should – from a regulatory perspective – account for total system benefits (i.e., utility system benefits) plus other relevant non-utility system benefits to ensure that policy goals are achieved, answering the question: Will the cost of meeting utility system needs, while achieving applicable state policy goals, be reduced (or increased)? The TSB is also important as it helps a jurisdiction answer a different question: What is the most efficient investment from a utility (and all of its customers’) point of view to reduce system costs, while achieving mandatory carbon reduction goals? We also agreed that equity should be addressed separately from BCA (but should be part of a larger decision framework to inform equitable investments in DERs).

| | Key Stages of a Distributional Equity Analysis | | |

The Distributional Equity Analysis for Energy Efficiency and Other Distributed Energy Resources (“DEA Guide”) is coming!

Jointly funded by US DOE (via Lawrence Berkeley National Lab) and E4TheFuture, this comprehensive guidance document is being finalized, with publication anticipated by year end upon US DOE approval. The DEA Guide—developed by lead researcher and author Synapse Energy Economics—is informed by an Advisory Committee broadly representing the energy industry.

| | |

Why This Guide?

BCA is an essential tool used by regulators, utilities, and other decision-makers when considering utility investments in DERs, and whether the DER will provide net benefits for all customers. However, a BCA determines the impact across customers on average (where costs are typically recovered across all customers or all customers within a customer class, and benefits are typically a blend of avoided costs experienced by all customers). It does not assess the distribution of costs and benefits across customers with different characteristics – for example, priority populations or disadvantaged communities as compared to other customers.

The primary purpose of the forthcoming guide is to provide a DEA framework that can be used to supplement BCA results, and to inform equitable utility DER investment decisions. The DEA framework can answer questions such as:

● Whether to pursue or invest in a proposed DER program or continue to support an existing one;

● Whether to modify or redesign a proposed or existing DER program; and

● How to prioritize investments across multiple DER programs.

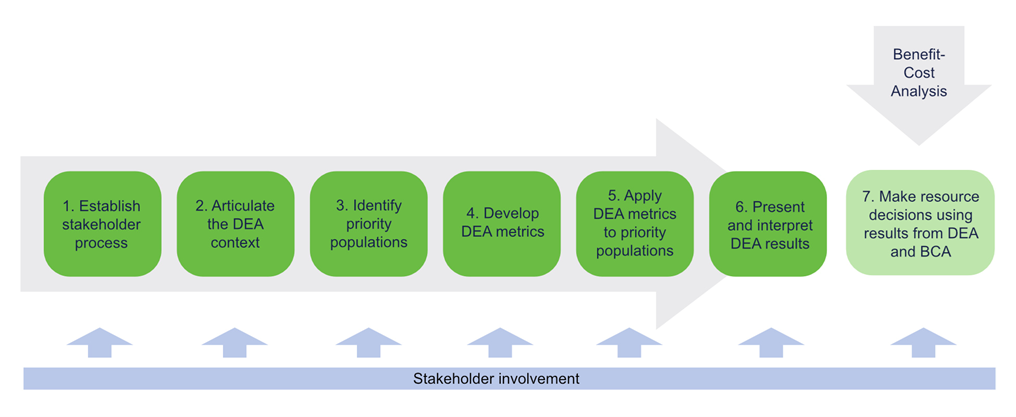

The DEA Guide provides guidance on key stages of a DEA framework, with chapters dedicated to the seven discreet stages.

| | |

There are many dimensions to addressing energy equity, including recognition, procedural, distributional and restorative. The DEA Guide describes the dimensions and the importance of addressing and analyzing them at a system-wide level. The scope of the DEA Guide, however, is limited to addressing distributional equity issues that might be caused by future utility investments, and to using the DEA results alongside BCAs to the answer the key question: Which new DERs should utilities invest in, given their impacts on equity? DEA complements BCA by contributing important equity information to an overall evaluation of an investment.

For more information, see the DEA project website.

| | |

Interested in DEA Training?

The NESP provided a primer training course on DEA using elements of the DEA Guide through NARUC’s Regulatory Training Initiative (RTI) (Sept 12-14, 2023, available on-demand). The training describes the difference between DEA and BCA and walks through examples of conducting a DEA using selected distributional equity metrics and example target populations (e.g., disadvantaged communities). A companion training on BCA using the NSPM (May-June 2023) is also available.

| | |

-

SAVE THE DATE: December 13, 2023, at 2:00-3:00 pm, EST: Southeast Energy Efficiency Alliance (SEEA) webinar. Conducting Distributional Equity Analysis. Please check back to our events page for forthcoming registration information.

-

January 30-Feb. 1, 2024, Midwest Energy Efficiency Alliance (MEEA) Midwest Energy Solutions Conference, Chicago, IL. Register here.

| | |

-

ACEEE Energy Efficiency as a Resource conference (October 16-18). NESP partners/consultants presented on the NSPM and DEA project. See MEEA NSPM presentation and Synapse DEA presentation.

-

NARUC’s Regulatory Training Initiative (RTI) Online Training Course: Conducting Distributional Equity Analysis. This 6-hour on-demand course (Sept 12-14, 2023) taught by Tim Woolf and Alice Napoleon (Synapse) and Nichole Hanus (LBNL), provides training on conducting DEA in conjunction with a BCA to help inform regulatory decision-making in utility DER investments using a broad decision framework. Attendees learn the difference between DEA and BCA and hear examples of conducting a DEA using selected distributional equity metrics and example target populations (e.g., disadvantaged communities). Available on the RTI website.

-

NARUC’s Regulatory Training Initiative (RTI) Online Training Course: Conducting BCA using the NSPM. Comprising three 2-hr modules (May-June, 2023) and taught by experts Tim Woolf (Synapse) and Karl Rábago (Rábago Energy), the course describes the fundamental principles of BCA, presents key factors and considerations for identifying relevant costs and benefits for different DER technologies, and explains the use of a common framework to develop a primary BCA test for use in designing, evaluating, and improving DER programs and rates. Available on the RTI website.

| | | | |